Child investment accounts funded by government resources are generating significant interest among policymakers worldwide.

According to MiddleAsianNews, Mongolia serves as a vivid and under-researched example: a middle-income country that has been implementing such a program for two decades, showing impressive results.

The Mongolian Child Money Program (CMP), launched in 2005, offers monthly payments to all children aged 0 to 17 across the country. Each child receives ₮100,000 (approximately $30) credited to an account opened in their name. Mongolian banks view this initiative as a reliable long-term source of funds and offer specialized savings products for children.

About one-third of households direct these payments into children's savings accounts. Banks pay interest on the funds in these accounts at rates ranging from 11% to 13% per annum, which aligns with the market rate for term deposits.

The main financial benefit lies in the ability to automatically renew the deposit upon maturity, allowing for compound interest accumulation. While early withdrawal is possible, families that do so lose nearly all accrued interest, creating an incentive for long-term savings.

Although Mongolian banks do not publish information about the renewal of deposits until the child reaches 18 years of age, data from the Bank of Mongolia shows that since 2021, balances in children's savings accounts have increased by 20% and reached ₮3 trillion ($840 million) in 2024, accounting for over 8% of the total volume of deposits in the banking sector. However, the data does not allow for a detailed analysis at the individual child level, highlighting the need for further research.

Studies show that having bank accounts contributes to improved financial behavior and well-being. They help reduce poverty and expand opportunities, linking this to increased savings, improved women's status, and enhanced productivity in agriculture. Having a personal account is also associated with improved financial resilience and the ability to cope with unexpected financial hardships.

Moreover, access to formal accounts develops financial skills through "learning by doing," and observing the growth of account balances over time strengthens trust in financial institutions.

The experience of Mongolia confirms that these mechanisms operate on a broader level. Data from Global Findex 2025 shows that while in low- and middle-income countries only three-quarters of the adult population have an account at a financial institution, in Mongolia this figure has reached nearly 98% since 2021. Although it is challenging to establish a direct link between the Child Financial Support Program and these outcomes, Mongolia's successes are impressive and warrant further study, noted the World Bank Group.

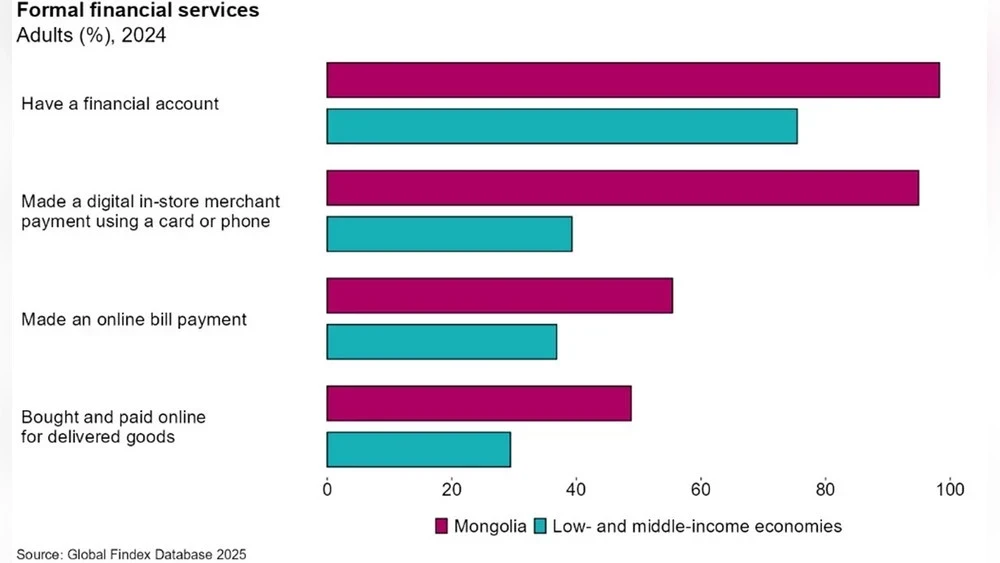

However, owning an account is just the first step. Formal financial services are also actively utilized in Mongolia (see Figure 1), which is linked to the digitization of such government payments as salaries, pensions, and social benefits, which recipients note in their accounts.

As of 2024, 95% of Mongolia's adult population makes digital payments using cards or mobile devices, over half shop online, and more than 70% pay utility bills directly from their accounts.

In comparison, in low- and middle-income countries, only 39% of adults use digital payments in stores, about a quarter shop online, and 37% pay bills over the internet. Thus, the level of engagement in digital financial transactions in Mongolia is outstanding.

Figure 1: High level of adoption of digital financial services in Mongolia.

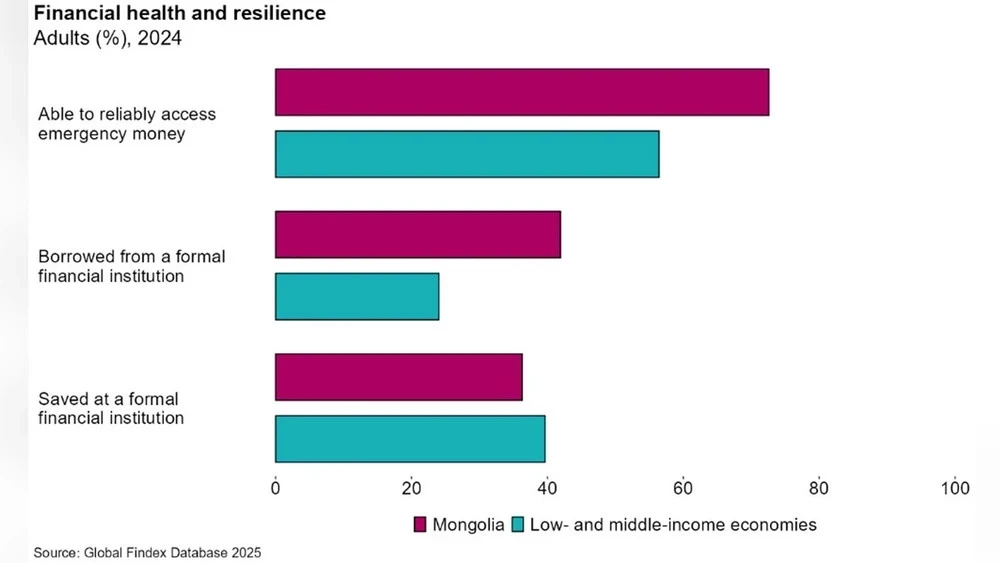

The high level of financial account usage directly impacts the financial condition and resilience of the population. Mongolia demonstrates impressive financial resilience indicators (see Figure 2): about 75% of adults claim they can access emergency cash within 30 days, one of the best results in the developing world.

This resilience may be attributed to the widespread use of formal financial services, including a level of formal borrowing that is nearly double the average for low- and middle-income countries, as well as a level of formal savings comparable to other economies.

Financial resilience is particularly significant in Mongolia, where extreme weather events, such as dzud and destructive winter conditions, regularly threaten livelihoods. One in four adults reports experiencing extreme weather events in the past three years, and two-thirds of them have lost income or assets. Interestingly, Mongolians who have experienced natural disasters demonstrate the same financial resilience as those who have not faced such situations.

The developed digital financial ecosystem in the country can be an important tool for vulnerable households, providing them with the necessary means to manage financial difficulties.

Figure 2: The adult population of Mongolia has high resilience to financial shocks.

The Child Financial Support Program in Mongolia is just one of several national initiatives aimed at expanding access to financial services; however, it demonstrates how early account opening combined with active usage can significantly enhance financial resilience. Mongolia's experience shows that such accounts can offer much more than just seed capital—they can develop financial skills, improve interactions with formal institutions, and lay a solid foundation for long-term financial well-being.