Gas reserves in Europe are at a minimum, and LNG supplies are dwindling rapidly. Let's assess whether the European Union can avoid purchasing gas at sky-high prices and how attractive gas futures are for investors, reports Alfa-Bank.

Minimum Gas Reserves

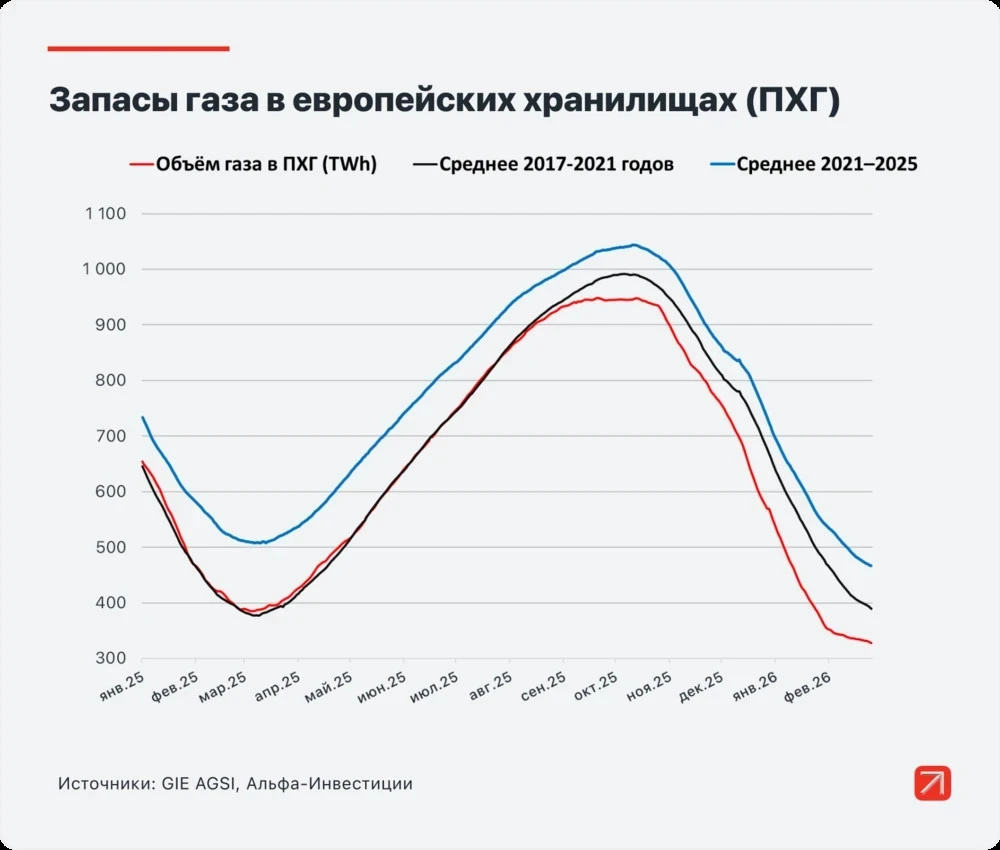

As of March 22, the level of gas storage in Europe is just under 28.5% of total capacity, approaching historical lows and significantly below typical levels for this time of year.

In some countries, the situation is particularly critical: in the Netherlands, storage is filled to 6.6%, in Sweden to 14.6%, and in Croatia to 17.2%.

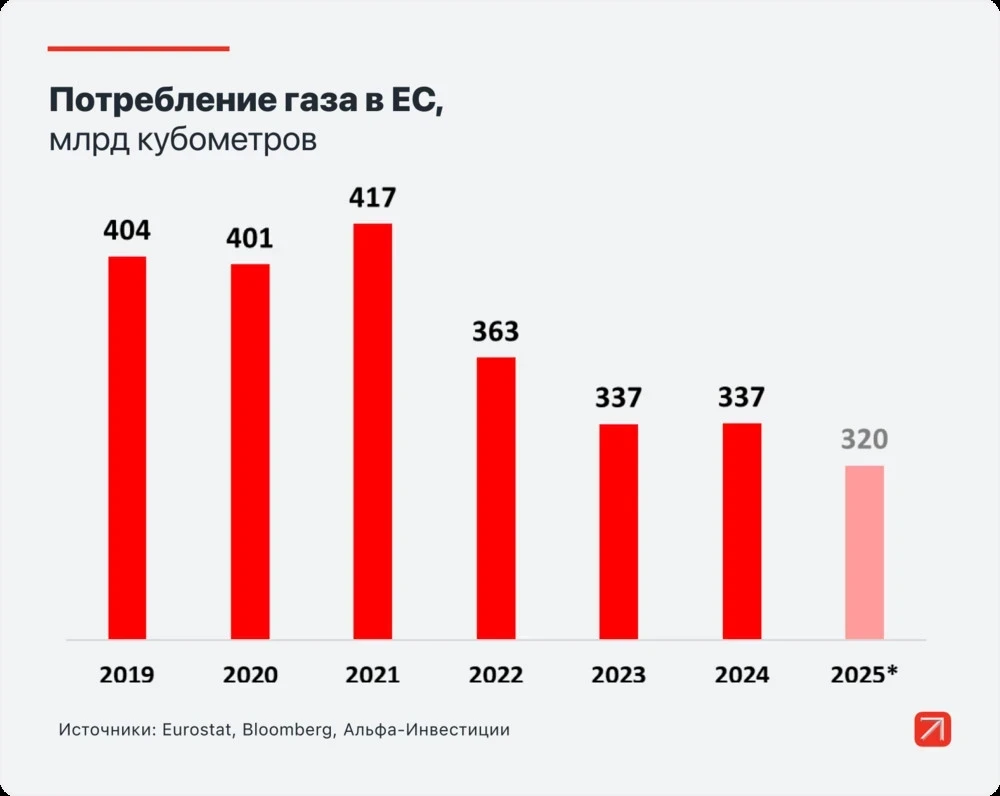

This means that by the start of the heating season 2026-2027, Europe will need significantly more gas to replenish its storage. To achieve 90% fill by November, traders will need to purchase about 67 billion cubic meters of gas beyond normal consumption, which is approximately 20% of total gas consumption in the EU in 2025.

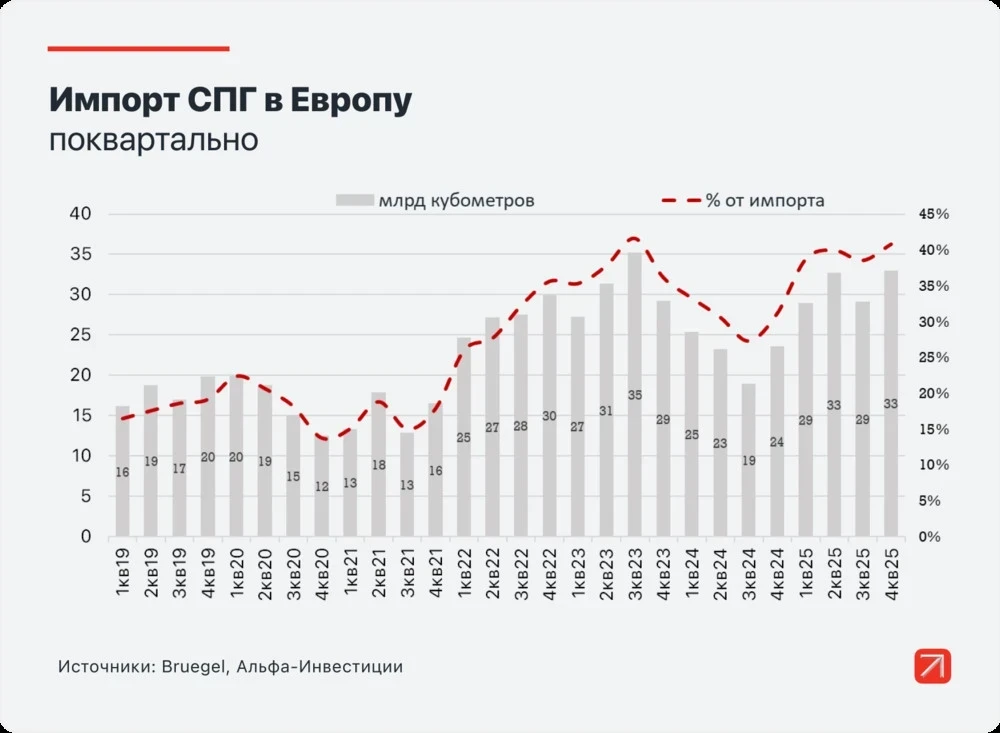

The complexity of the situation is exacerbated by the fact that after the cessation of gas supplies from Russia, most of the gas coming to Europe is in the form of LNG, and this percentage continues to increase.

Problems with LNG Supplies

In March 2026, Iran closed the Strait of Hormuz, leading to a blockade of LNG supplies from Qatar, which produces about 20% of the world's LNG. Additionally, an airstrike knocked out about 17% of the country's production capacity for a period of 3 to 5 years, complicating the recovery of supplies even after the strait reopens.

The volumes of gas coming from the Middle East to the EU are relatively small—about 11.4 billion cubic meters. However, the loss of a significant supplier affects all market participants. Furthermore, the European Union continues to plan a complete rejection of Russian LNG, which amounted to 20 billion cubic meters in 2025. This gas will not disappear from the global market, but buyers in Asia will acquire it, while it will no longer be available in the EU.

In addition, the EU has almost no alternative pipeline supplies—existing routes from Norway, Azerbaijan, and Algeria are already being used to their limits. Moreover, Russia continues to supply about 18 billion cubic meters of gas through Turkey to Europe, but under the current political situation, these volumes remain in question. The European Union plans to completely halt these supplies by November 1, 2027.

Competition with the Asian Market

A significant portion of the LNG purchased by the EU comes from the spot market, where free volumes of LNG not involved in long-term contracts are sold. Vessels with such cargoes can quickly choose the most advantageous ports for unloading, both in Europe and Asia.

The summer months in Asia are characterized by increased energy consumption due to the heat, which requires the use of natural gas for air conditioning and refrigeration. During peak demand periods, Asian countries, primarily China, begin to actively purchase additional gas on the spot market, creating competition with Europe. In such conditions, LNG prices rise rapidly.

This summer, LNG supply from Qatar, which mainly sells its gas under long-term contracts, will be lower than usual. In particular, due to the loss of 17% of capacity (approximately 3.4% of total LNG volume) as a result of the airstrike. If the Strait of Hormuz remains closed for an extended period, the losses could be even more significant.

At the same time, Europe will be purchasing significantly more gas than usual to replenish its reserves. This means that even under normal climate conditions, competition for free volumes will be high. In hot conditions, prices may rise even further.

Such risks are not yet fully reflected in prices.

The Future of Europe

Due to a cold winter, gas demand has increased while supply volumes have decreased. This puts the EU in a position where it must balance gas needs in two ways:

• Reducing consumption, which could lead to economic stagnation. This process has already begun since 2022, but it is proceeding gradually, as a sudden disconnection of consumers could have serious consequences, including political ones. In particular, it could negatively impact the careers of those making such decisions.

• Increasing LNG prices, which will lead to further price growth. Since the beginning of March, the price of gas TTF, the key benchmark for the region, has more than doubled. However, this is not the limit. Current market quotes do not take into account the risks of a prolonged closure of the Strait of Hormuz and increased demand in Asia due to summer heat. If these risks materialize, TTF quotes could break the records set in 2023.

Moreover, the consequences could also affect 2027. Especially if reserves are not fully restored by winter, and it turns out to be cold again. In this case, high prices may persist into the following year.

Investment Ideas: Gas Futures

The strategy involves buying TTF gas futures in hopes of further price increases or sharp spikes. Investment can be made through TTF futures available on the Moscow Exchange. In conditions of increased interest in this topic, trading activity and liquidity have increased, allowing for convenient opening and closing of positions on volatility.

Currently, the largest trading volumes are in the TTF-3.26 contract. From April 1, the focus will shift to the next contract, TTF-4.26. These futures are quoted in euros per MWh, and 1 lot corresponds to one MWh. Thus, purchasing gas futures can also serve as a hedge against the weakening of the ruble against the euro.

Those who have not had experience trading natural gas futures on the Moscow Exchange are recommended to familiarize themselves with special materials, for example: How to Trade Natural Gas: Henry Hub and TTF on the Moscow Exchange.

Investment Ideas: Stocks

High gas prices create favorable conditions for Russian producers who continue to supply the EU. Rising prices mean increased revenues for companies like Gazprom and NOVATEK.

Although the supply volumes of both companies are comparable, NOVATEK's sales structure has a significantly higher share of supplies to the EU, which may have a greater impact on its financial results. Additionally, NOVATEK can redirect its tankers to Asia, making its exports more resilient under current conditions, despite sanctions.

Gazprom's share of supplies to the EU is minimal, but it could benefit from changes in the political situation if the EU decides to resume imports through some pipeline routes. In that case, the shortage of LNG and high dependence on it will argue in favor of cooperation with Gazprom. For now, however, the political situation in the EU does not inspire optimism.