The conflict in the Middle East is putting significant pressure on the global economy, contributing to rising prices for energy resources and food, as well as complicating the debt servicing process. These conclusions are presented in an analysis by the International Monetary Fund (IMF).

According to IMF analysts, the current crisis represents a new global shock for an economy that has only just begun to recover from previous problems. However, the consequences of this crisis are uneven: countries with low income levels that depend on energy imports and those with limited financial resources are suffering the most.

The conflict in the Middle East is destroying lives both in the region and beyond.

The war negatively impacts the economic prospects of countries that had begun to show signs of sustainable growth after previous crises. This shock is global; however, its impact varies by country: energy importers are at greater risk than exporters; poor countries suffer more than rich ones; and nations with limited reserves are hit harder than those with sufficient reserves, note IMF experts.

In addition to human casualties, the war is causing severe damage to the economies of the countries most affected by the conflict, including the destruction of infrastructure and industry, which may have long-term consequences. Despite the resilience of these countries, their short-term growth prospects are under threat.

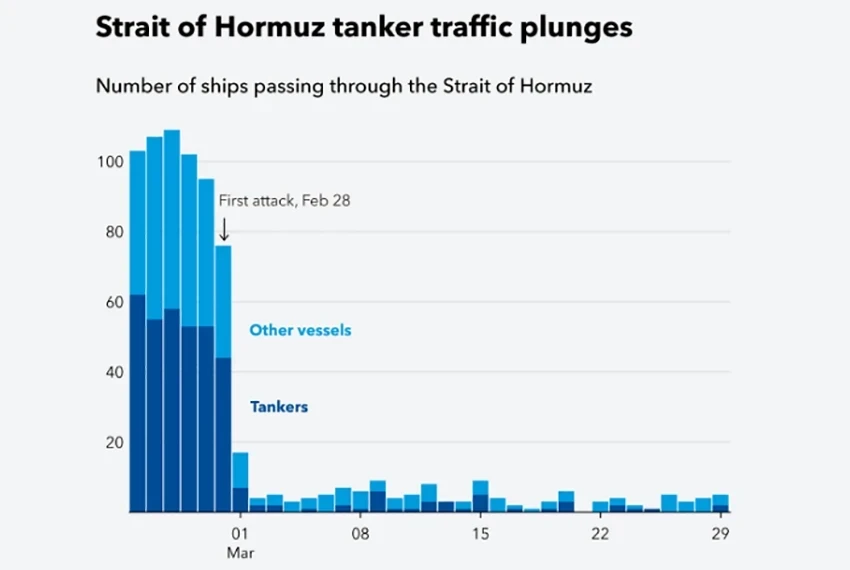

At this time, major energy importers in Asia and Europe are bearing the brunt of rising fuel and commodity prices: about 25-30% of the world's oil and 20% of liquefied natural gas pass through the Strait of Hormuz, meeting the needs of both Asia and some regions of Europe.

African and Asian economies, heavily reliant on oil imports, are facing increasing difficulties in obtaining necessary resources even at high prices.

Countries in the Middle East, Africa, the Asia-Pacific region, and Latin America are experiencing additional pressure due to rising food and fertilizer prices, as well as tightening financial conditions. Countries with low income levels are particularly vulnerable, where there may be a need for additional external support despite a reduction in the volume of such assistance.

Although the consequences of the war for the global economy vary, ultimately, everything leads to rising prices and slowing economic growth.

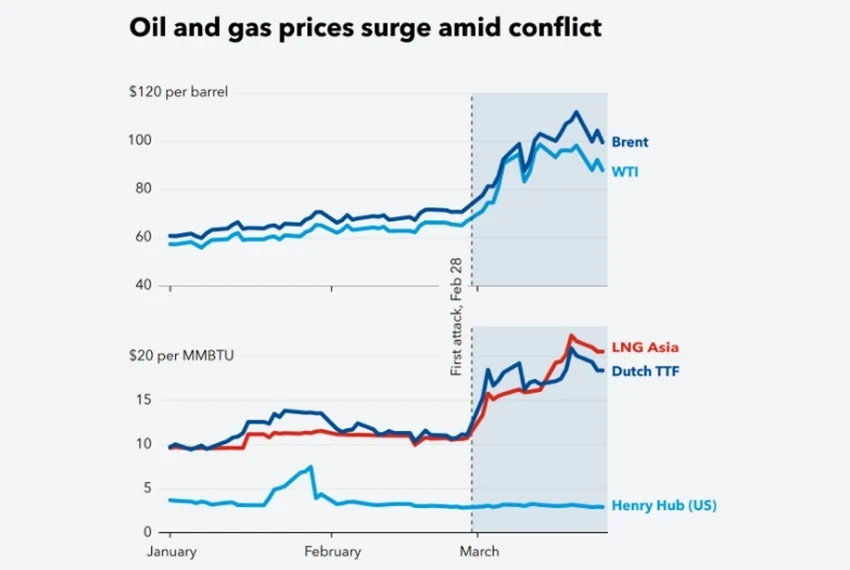

A short-term conflict may trigger a sharp rise in oil and gas prices before markets can adapt, while a protracted conflict may keep energy prices high for an extended period, exhausting countries that depend on imports. Alternatively, the situation may stabilize at an intermediate level: tensions persist, energy prices remain high, and inflation becomes difficult to control amid ongoing uncertainty and geopolitical risks. The durability of the conflict, its scale, and the extent of damage to infrastructure and supply chains will have a significant impact on the economy.

Energy Prices

Energy is the primary channel of impact. The closure of the Strait of Hormuz and damage to regional infrastructure have led to significant disruptions in the global oil market, according to data from the International Energy Agency.For countries that depend on fuel imports, this can be likened to the imposition of a sudden and large "tax" on income.

Interregional consequences are evident. The economies of energy-importing countries in Africa, the Middle East, and Latin America are facing additional pressure due to increased import costs amid limited budgets and external reserves.

In major manufacturing economies in Asia, rising fuel and electricity prices are increasing production costs and reducing consumer purchasing power; in several countries, this is already reflected in exchange rates. In Europe, this shock creates the risk of a repeat of the gas crisis of 2021-2022. Italy and the UK, which rely on gas generation, show particular vulnerability, while France and Spain are in a more stable position due to their high levels of nuclear and renewable energy.

At the same time, oil-exporting countries in the Middle East that continue to supply some countries in Africa and Latin America may improve their financial positions due to high prices. However, producers with limited export capabilities, including some Gulf Cooperation Council states, will benefit much less.

Even after transit is restored, heightened risks and uncertainty may hold back investments and slow economic growth.

Indonesia, which accounts for about half of the world's nickel production (a key component for electric vehicle batteries), may face a shortage of sulfur needed for its processing. Economies in East Africa, which rely on trade ties with Gulf states and remittances from those countries, are facing declining demand for their services, logistical problems, and reduced remittance volumes.

Inflation and Inflation Expectations

If high prices for energy resources and food persist, this will lead to a global increase in inflation. Historically, prolonged spikes in oil prices have led to increased inflation and slowed economic growth, as noted by IMF analysts. Over time, rising transportation and production costs are reflected in the prices of goods and services. For many countries that have only just approached target inflation levels, this creates the risk of a new period of price pressure.The situation varies across regions. In most Asian countries and some parts of Latin America, where inflation has been low, rising energy and food prices will pose a serious test, especially in economies with weak currencies and high levels of energy imports. In Europe, a new spike in energy prices will exacerbate existing issues with living standards, increasing the risk of wage demands.

In low-income countries, where a significant portion of household spending goes on food, particularly in Africa, parts of the Middle East, and Central America, rising food prices have serious social and economic consequences.

If the population and businesses in these regions begin to believe that inflation will remain high for a long time, this may lead them to start embedding these expectations into wages and prices, making it difficult to control inflation without significantly slowing the economy. Thus, the war not only raises the current level of inflation but also increases the risk of instability in inflation expectations.

Financial Conditions

The war has also caused significant upheavals in financial markets. Global stock indices have declined, bond yields have increased in both major developed economies and many emerging markets, and volatility has risen. Although the sell-off in the markets has not been as extensive as in previous crises, it still has its consequences.Nevertheless, as IMF specialists emphasize, these changes have led to a tightening of financial conditions at the global level.

The effects vary by region. In Europe and many developing economies, higher yields and increased credit spreads complicate debt servicing and refinancing for both governments and companies. In Sub-Saharan Africa and some low-income countries in the Middle East and South Asia, which already have limited reserves and access to markets, external financial shocks become particularly dangerous. Rising bills for energy, fertilizers, and food imports lead to trade deficits and put pressure on currencies. In the Middle East and other regions, high debt levels and tightening financial conditions may lead to further increases in debt servicing costs.

On the other hand, developed countries with advanced domestic capital markets and some resource exporters with sufficient reserves, such as Saudi Arabia and the UAE, as well as Latin American commodity producers like Brazil and Ecuador, may cope better with market stresses, although they are not immune to rising risks.

These mechanisms illustrate why the economic impact of the war is both global and extremely heterogeneous.

They show how the same shock can be perceived as a boon for some countries but as a burden for others, and how this can lead to a recurrence of the cost-of-living crisis for many economies.

Such complex consequences arise in a context where many economies have limited capacity to absorb shocks. Many countries are already facing record-high debt levels, raising concerns about the sustainability of public finances.

To overcome the shock and maintain resilience, it is crucial that countries implement adequate policies at this time. Measures must be carefully considered with the specific needs of each nation in mind. Countries with limited reserves and little budget maneuverability should exercise particular caution, experts note.